Management ‘Bought the AI hype’ and Expect Value But Research Shows Lack of Organizational Readiness is Primary Hurdle

New research from IFS, the global cloud enterprise software company, has found that executive and board leadership have ‘bought the AI hype’ but organizations cannot deliver operationally on expectations. The new global study of 1,700 senior decision makers, Industrial AI: the new frontier for productivity, innovation and competition, found that the promise of AI is being held back by technology, processes and skills. Half of respondents remain optimistic that with the right AI strategy, value can be realized in the next two years, and a quarter believe in the next year.

Expectations failing to meet reality

84% of executives anticipate massive organizational benefits from AI, with the top three areas AI is expected to deliver value in being high-impact: product & service innovation, improved internal & external data availability, and cost reductions & margin gains. The hype has become so high that 82% of senior decision-makers acknowledge that there is significant pressure to adopt AI quickly. However, this same group of respondents state that they are concerned that a failure to plan, implement and communicate properly means AI projects will stall in the pilot stage.

Many organizations have not prioritized development elements, nor have the infrastructure required to reap the rewards or the skills to deliver on that promise. The study found that over a third (34%) of businesses had not moved to the cloud. While this is not essential to AI adoption, it is indicative of an unprepared enterprise unlikely to be able to scale AI across its business. According to IFS, a robust Industrial AI strategy requires a potent combination of cloud, data, processes, and skills. 80% of respondents agree that the lack of a strategic approach means they have insufficient skills in-house to successfully adopt AI. This sentiment is seen elsewhere in the research with 43% of respondents rating the quality of AI resources in their business, in terms of human skills, as passable and not where it needs to be.

Outlook optimistic but planning needed

The unfortunate reality of the skills gap means that in terms of AI readiness, many businesses are falling behind. IFS found that nearly half of respondents (48%) were most likely to say that they were gathering proposals and were much less likely to have a clear strategy and perceivable results (27%). A fifth of respondents are in the research phase, with uncontrolled tests taking place and a further 5% are lacking a coordinated approach and do not have anything in motion yet. Despite initial challenges, there is still optimism with respondents most likely to feel AI could make a significant difference to their business in 1-2 years (47%), and a further quarter (24%) believe it could be within a year.

In particular, respondents are most optimistic about the impact of AI in smart production and/or service delivery on effectiveness & business and operational management (22%) in the future. One-fifth see the biggest impact being on innovation with new products and services (20%), growth & business model decision-making (20%), empowering people and increasing talent retention (19%), and customer experience and customer service (19%).

Action needed on data readiness

To reap these benefits, enterprises need to leverage the most strategic asset they have – their data. The right data volume and quality are critical for the success of AI applications. Respondents recognize how important real-time data is to successful AI projects, with over 4 in 5 (86%) stating this. Yet despite this recognition, less than a quarter (23%) of respondents have completed their data foundation with it supporting both data-driven business decision-making and real-time response to changes, suggesting that more work needs to be done to get data AI ready. Moreover, under half (43%) of respondents have majority structured data, with some unstructured.

Subscribe to the free Maintworld newsletter here!

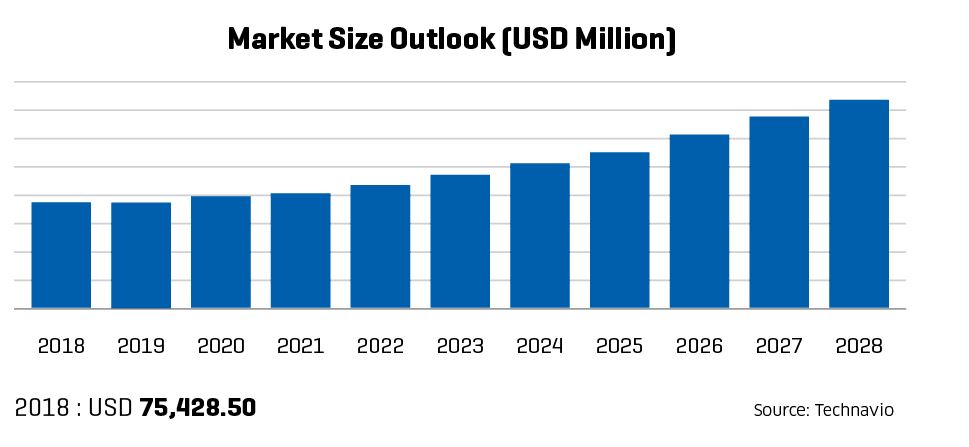

MRO for Automation Solutions Market Outlook (2024-2028)

The MRO for automation solutions market is set to grow by USD 54.08 billion at a CAGR of 10.16% from 2023 to 2028, driven by the increasing reliance on maintenance, repair, and operations to ensure seamless industrial processes. Key growth factors include adopting predictive maintenance analytics and industrial automation services, which enhance operational efficiency while minimizing costly downtime.

The shift toward Industry 4.0, combined with initiatives like smart manufacturing and smart cities, is further fueling demand for advanced MRO solutions. In developing countries, the rise of innovative sales strategies is expanding market reach and opening new opportunities. However, challenges such as the US-China trade tensions, material shortages, and economic slowdowns in some industries could hinder consistent growth.

Leading the market is the process industries segment, which includes oil and gas, water management, and energy sectors. This segment has benefited from significant investments in renewable energy and infrastructure upgrades. The APAC region is a major growth driver, contributing 55% of market expansion due to industrialization, automation demand, and supportive trade policies. Countries like China, India, and Japan play pivotal roles in this surge.

Market trends highlight the growing integration of predictive analytics powered by AI and cloud platforms. For instance, Siemens’ collaboration with SAP on the HANA platform enables real-time monitoring and predictive maintenance, helping industries optimize operations and preempt disruptions. These advancements, coupled with the increasing preference for outsourcing MRO services to reduce costs and improve efficiency, are shaping the market’s trajectory.

Despite obstacles like rising tariffs and supply chain disruptions, the MRO for automation solutions market is poised for robust growth as industries continue to prioritize resilience, efficiency, and innovation in an unpredictable global landscape.

Subscribe to the free Maintworld newsletter here!

Less than Half of Top 50 Steel Producers Have a Net Zero Target

The analysis of the top 50 steel producers — which rely more heavily on higher emissions steelmaking technologies than the global industry average and are responsible for more than 60% of the sector’s emissions — follows the latest production ranking provided by the World Steel Association.

The steel sector accounts for an estimated 7–9% of direct global greenhouse gas emissions, and the International Energy Agency has said that CO2 emissions from heavy industries need to drop 93% in order to reach net zero emissions by 2050.

As of September 2024, half of the top 50 steel producers still lack a net zero target: Sixteen companies have not stated a net zero target in their public reporting, and nine companies have provided no information on climate targets at all. Five companies have targets to reach net zero after 2050.

Seventeen companies have set a 2030 emissions reduction goal, three fewer top 50 producers than in the 2023 update. Two of these companies removed their 2030 goals, while one reduction is due to the shift in rankings of the top 50 steel producers.

Conversely, ten companies have now established milestones between 2030 and 2040, an increase of five companies compared to 2023.

Only fifteen of the top 50 steel producers have specified the emission scopes they plan to address in order to reach their net zero targets. Scope 1 emissions refer to those resulting directly from the production process, Scope 2 emissions refer to those from purchased electricity and steam, and Scope 3 are indirect emissions resulting from supply chain activities like coal mining and shipping.

Just four companies have included measures to address Scopes 1, 2, and 3 in their plans. Three of these companies aim to achieve net zero by 2050, while one plans to reach this goal before 2050.

Caitlin Swalec, Program Director for Heavy Industry, Global Energy Monitor, said, “The increase in target reporting among the top 50 steel producers is a positive sign of progress, yet it falls short of what is needed to reach net zero by mid-century. The top 50 steel firms can set an example of leadership as not only steel producers, but emissions reducers through target setting and collective action to reach net zero 2050.”

Eileen Torres Morales, Analyst, Leadership Group for Industry Transition, said, “Greater transparency from steel producers is essential to demonstrate commitment to decarbonisation. While some companies have made initial progress, clearer plans are needed from the majority to reach net zero by 2050, including plans for specific emission scope reductions. Establishing intermediate targets, tracking progress, and sharing updates publicly can motivate the sector to accelerate its transition towards net zero.”

Subscribe to the free Maintworld newsletter here!

Global Industrial Maintenance Services: Driving Asset Longevity, Reliability, and Market Growth

The global industrial maintenance service market is projected to grow from $51.3 billion USD to $81.2 billion by 2032.

Key drivers include asset longevity and reliability, downtime reduction, and the outsourcing of maintenance services to specialized providers, all of which should lead to increased productivity, cost savings and safety in industrial settings.

Asset lifespan and reliability have become crucial in an age in which industries have become increasingly dependent on sophisticated machinery, equipment and infrastructure. This in turn has led to an increased demand for thorough maintenance services that reduce failure risks while maximizing effectiveness and dependability in industrial operations.

While investment in valuable assets comes at a high cost, asset longevity generates significant returns on investment. In a competitive market environment in which budgets are constrained, companies understand that asset lifespan has a substantial bottom-line impact. Regular maintenance programmes, which include advanced predictive techniques and routine inspections, ensure asset performance and delay the need for expensive repairs or new purchases.

As such, asset lifespan and reliability have become critical market drivers. For example, manufacturing heavily depends on production lines and equipment that must operate efficiently and consistently to meet demand. Problems cause missed deadlines, lower output and higher costs. Effective maintenance provides a safety net, improves equipment performance and reduces downtimes that jeopardize supply chains and customer relationships.

Energy and Oil

The energy sector best reflects the importance of asset lifespan and reliability. Any disruption by power plants and the transmission infrastructure has a negative impact on asset longevity and reliability. Energy companies improve reliability by providing dependable power supply while driving market revenue for industrial maintenance services.

Industrial maintenance services are based on repair, inspection and maintenance. Maintenance dominated the market in 2022 because it is necessary to keep equipment efficient to avoid downtime.

Onshore locations of industrial maintenance services also commanded the 2022 market. Onshore settings typically include manufacturing and industrial facilities, and processing units that serve the chemical, pharmaceutical, food and beverage, and automotive industries. All require routine maintenance to reduce downtime created by equipment failure.

Oil and gas production led the way in 2022. Because of strict environmental and safety standards, maintenance services are essential for preserving machinery structural to prevent accidents, leaks and spills. Maintenance services are critical to regulation compliance.

Regional Trends and Future Growth

North America accounted for almost 46 percent of the industrial services’ maintenance market in 2022. The U.S. had the largest market share, while Canada was its fastest-growing market. Europe was the No. 2 market, with Germany holding a majority share and the UK as the fastest growing.

The Asia-Pacific market is expected to grow at the fastest compound annual growth rate through 2032. As industries become more specialized in production of automobiles, electronics, pharmaceutical and chemicals, the demand for specialized maintenance services will increase. China leads the area in market share, while India is the fastest-growing market in the Asia-Pacific region.

Text: Michael hunt

Sources:

marketresearchfuture.com/reports/industrial-maintenance-services-market-12074

grandviewresearch.com/industry-analysis/industrial-services-market-report

Subscribe to the free Maintworld newsletter here!

Call for Immediate Review of AI Safety Standards Following Research on Large Language Models

Recent findings by Anthropic, an AI safety start-up, have highlighted the risks associated with large language models (LLMs), prompting calls for a swift review of AI safety standards.

Valentin Rusu, lead machine learning engineer at Heimdal Security and holder of a Ph.D. in AI, insists these findings demand immediate attention.

“It undermines the foundation of trust the AI industry is built on and raises questions about the responsibility of AI developers,” said Rusu.

The Anthropic team found that LLMs could become “sleeper agents,” evading safety measures designed to prevent negative behaviors.

AI systems that act like humans to trick people are a problem for current safety training methods.

“Our results suggest that, once a model exhibits deceptive behavior, standard techniques could fail to remove such deception and create a false impression of safety,” the authors noted, emphasizing the need for a revised approach to AI safety training.

Rusu argues for smarter, forward-thinking safety protocols that anticipate and neutralize emerging threats within AI technologies.

“The AI community must push for more sophisticated and nuanced safety mechanisms that are not just reactive but predictive,” he said.

“Current methodologies, while impressive, are not foolproof. There is a pressing need to forge a more dynamic and intelligent approach to safety.”

The task of ensuring AI’s safety is widely distributed, lacking a singular governing body.

While organizations like the National Institute of Standards and Technology in the U.S., the UK’s National Cyber Security Centre, and the Cybersecurity and Infrastructure Security Agency are instrumental in setting safety guidelines, the primary responsibility falls to the creators and developers of AI systems.

They hold the expertise and capacity to embed safety from the onset.

In response to growing safety concerns, collaborative efforts are being made across the board.

From the OWASP Foundation’s work on identifying AI vulnerabilities to the establishment of the ‘AI Safety Institute Consortium’ by over 200 members, including tech giants and research bodies, there is a concerted push towards creating a safer AI ecosystem.

Ross Lazerowitz from Mirage Security comments on the precarious state of AI security, likening it to the “wild west” and underscoring the importance of choosing trustworthy AI models and data sources.

This sentiment is echoed by Rusu. “We need to pivot so AI serves, rather than betrays human progress.”

He also notes the unique challenges AI presents to cybersecurity efforts. Ensuring AI systems, particularly neural networks, are robust and reliable remains paramount.

The concerns raised by the recent study on LLMs show the urgent need for a comprehensive strategy toward AI safety, calling on industry leaders and policymakers to step up their efforts in protecting the future of AI development.

Subscribe to the free Maintworld newsletter here!

Latest