The Industrial Machinery Remanufacturing Market Size is Estimated to Grow at a CAGR of 18.54% Between 2023 and 2028

The market size is forecast to increase by USD 482.43 billion. The growth of the market depends on several factors such as the rising demand for increasing asset utilization in manufacturing industries, the growing demand for customization in industrial machinery, and the rising demand for optimization of costs at the same service level from various organizations.

Most end-users of industrial machinery are changing their existing machinery and equipment to enhance machinery efficiency, reduce operational costs, and integrate all operational functions. Selecting appropriate industrial machinery helps in boosting operational efficiency and lowering energy consumption. The growing demand for increasing asset utilization in manufacturing industries will fuel the growth of the market during the forecast period. Industrial machinery manufacturers are providing remanufacturing and maintenance services that use technologies such as plasma arc welding, and laser cladding in order to solve this problem.

Furthermore, the cost associated with the replacement of components may be quite high and represents a huge cost burden for the machine operator/owner. Such factors are expected to propel the global industrial machinery remanufacturing market during the forecast period.

The OEM segment in the global industrial machinery remanufacturing market is a crucial and evolving aspect. OEMs are enterprises that design, manufacture, and sell original machinery and equipment. This segment is unique in that it mostly involves the manufacturers themselves, who are mainly recognizing the value of remanufacturing. Many OEMs are adopting sustainable practices to decrease waste and undervalue their environmental footprint.

The OEM segment was valued at USD 112.16 billion in 2018. Furthermore, remanufacturing permits OEMs to deliver cost-effective solutions to customers, raising the affordability of their products and services. This can be particularly appealing in competitive markets. Besides, as regulatory pressures and environmental consciousness continue to increase, this segment is anticipated to deliver growth opportunities for both OEMs and remanufacturers in the market during the forecast period.

APAC is estimated to contribute 40% to the growth by 2027. Due to factors such as rapid industrialization and urbanization, APAC is the fastest-growing regional market in the global industrial machinery remanufacturing market. The leading countries in this region are China, Singapore, and India. APAC’s rapid economic development, particularly in countries like China and India, has led to increased industrialization, creating a substantial market for remanufactured machinery. As industries expand, the demand for cost-effective, reliable machinery solutions grows.

Moreover, several industries such as food and beverages, automotive, and others in the region are increasingly focused on sustainability and cost-effectiveness. Therefore, remanufacturing is seen as a waste reduction strategy adopted by several industry sectors. Thus, the rising adoption of sustainability practices in the region will drive the growth of the regional market during the forecast period

Source: Technavio report: Industrial Machinery Remanufacturing Market Analysis APAC, North America, Europe, Middle East and Africa, South America – US, China, India, Germany, UK – Size and Forecast 2024-2028

Subscribe to the free Maintworld newsletter here!

EU invests €216 million to promote semiconductor research and innovation

The Semiconductor Joint Undertaking (Chips Joint Undertaking) announced in February the launch of a €216 million call for proposals to support research and innovation initiatives in semiconductors, microelectronics and photonics.

This announcement follows the first round of calls for proposals for innovative pilot lines announced in November 2023, which attracted €1.67 billion in EU funding. Consortia can submit proposals on topics related to a wide range of challenges identified in the Strategic Research and Innovation Agenda – from silicon transistors to embedded artificial intelligence, connectivity or the coordination and control of complex systems to improve performance and safety.

In addition, projects funded under these new calls will contribute to the development of open source hardware for the automotive industry, support the transition to software-driven vehicles and promote environmentally friendly manufacturing processes. A specific joint call with the Republic of Korea will promote heterogeneous integration and neuromorphic (brain-like) computing.

Subscribe to the free Maintworld newsletter here!

Aiming for Emission-Free Pulping

The forest industry, technology companies, research organizations, and universities have joined forces to revolutionize the traditional pulping processes under the joint leadership of VTT Technical Research Centre of Finland and RISE Research Institutes of Sweden.

The Emission Free Pulping research program intends to find ways to improve energy efficiency, enhance the efficiency of wood usage and conversion to products, achieve emission-free pulping (especially carbon dioxide emissions), and significantly reduce water usage in the processes.

So far, five industrial companies have committed to the program, and they will bring in their knowledge about industrial relevance and operations as well as financial contribution. ANDRITZ, Arauco, Metsä Group, Stora Enso, and Valmet have committed to a five-year collaboration with the research organizations and universities for this program. The project involves significant contributions from Aalto University, Chalmers University of Technology, KTH Royal Institute of Technology, LUT University, Mid Sweden University, University of Helsinki, University of Oulu, and Åbo Akademi University.

“Technology plays one key role in the evolution of the pulp and paper industry. This transformation is not just about meeting industry standards; it’s about setting new benchmarks for environmental responsibility and operational excellence. The focus needs to remain on innovation and collaboration to drive this vital change in the industry,” concludes Johan Engström, CTO, ANDRITZ.

Subscribe to the free Maintworld newsletter here!

Sodium-ion Batteries Offer Promising Technology

The development of new battery technologies is moving fast in the quest for the next generation of sustainable energy storage – which should preferably have a long lifetime, have a high energy density and be easy to produce.

The research team at Chalmers chose to look at sodium-ion batteries, which contain sodium – a very common substance found in common sodium chloride – instead of lithium. In a new study, they have carried out a so-called life cycle assessment of the batteries, where they have examined their total environmental and resource impact during raw material extraction and manufacturing.

“The materials we use in the batteries of the future will be important in order to be able to switch to renewable energy and a fossil-free vehicle fleet,” says Rickard Arvidsson, Associate Professor of Environmental Systems Analysis at Chalmers.

“We came to the conclusion that sodium-ion batteries are much better than lithium-ion batteries in terms of impact on mineral resource scarcity, and equivalent in terms of climate impact. Depending on which scenario you look at, they end up at between 60 and just over 100 kilogrammes of carbon dioxide equivalents per kilowatt hour theoretical electricity storage capacity, which is lower than previously reported for this type of sodium-ion battery. It’s clearly a promising technology,” says Rickard Arvidsson.

The study is a prospective life cycle assessment of two different sodium-ion battery cells where the environmental and resource impact is calculated from cradle to gate, i.e. from raw material extraction to the manufacture of a battery cell. The functional unit of the study is 1 kWh theoretical electricity storage capacity at the cell level.

Both types of battery cells are mainly based on abundant raw materials. The anode is made up of hard carbon from either bio-based lignin or fossil raw materials, and the cathode is made up of so-called “Prussian white” (consisting of sodium, iron, carbon and nitrogen). The electrolyte contains a sodium salt. The production is modelled to correspond to a future, large-scale production. For example, the actual production of the battery cell is based on today’s large-scale production of lithium-ion batteries in gigafactories. The article Prospective life cycle assessment of sodium-ion batteries made from abundant elements has been published in the Journal of Industrial Ecology.

Subscribe to the free Maintworld newsletter here!

Study Reveals Widening Gap Between Organizations Benefiting from Digital Trust and Those Losing Out

DigiCert released its 2024 State of Digital Trust Survey that checks in on how enterprises around the world are managing digital trust in their organizations. While digital trust overwhelmingly remains a critical focus for all enterprises, the latest report shines a light on the growing divide between the ‘leaders’ –those who are getting it right, and the ‘laggards’ — those who are struggling.

The difference between leaders and laggards revealed some clues and potential best practices when it comes to digital trust. The top 33% digital ‘trust leaders’ enjoyed higher revenue, better digital innovation and higher employee productivity. They could respond more effectively to outages and incidents, were generally better prepared for Post Quantum Cryptography and were more readily taking advantage of the benefits of the IoT. Meanwhile, the bottom 33% ‘laggards’ performed comparatively poorly in all those categories and found it harder to reap the benefits of digital innovation. In addition, the leaders were more likely to centrally manage their certificates, more likely to employ email authentication and encryption (S/MIME) technology, and generally employed more mature practices in digital trust management.

The 2024 survey included a series of questions to determine how well (or poorly) each respondent was doing across a wide range of digital trust metrics. After the scores were totaled, the respondents were split into three groups: leaders, laggards, and those in the middle. Comparing the results between leaders, laggards, and those in the middle, notable differences emerged: Leaders exhibit far fewer issues on core enterprise systems (no system outages, few data breaches, and no compliance or legal issues) and experienced no IoT compliance issues, whereas half (50%) of the laggards did so.

Leaders also have significantly fewer issues due to software trust mishaps–for example, none of the leaders experienced compliance issues or software supply chain compromises, compared to 23% and 77% of the laggards, respectively. “As the threat landscape continues to expand, so does the gap between organizations who are leading the way in digital trust and those who are falling behind,” said Jason Sabin, CTO at DigiCert.

“Those who fall within the ‘leaders’ group and those who are a ‘laggard’ are well aware of who they are. The danger, however, is those organizations who fall in the middle and are not taking action due to a false sense of security.” Dallas-based Eleven Research administered the survey to 300 IT, Information Security and DevOps senior and C-level managers from enterprises with 1,000 or more employees in North America, Europe, and APAC.

Subscribe to the free Maintworld newsletter here!

Robotic Welding Matches and can Outperform Manual Construction

A new study has found improved fatigue performance, through standardised high-quality welding conducted by robots, could enable offshore wind jacket foundations to last longer or potentially to use less steel, thus having the potential to reduce the weight and cost of the structures.

The analysis, conducted by the Belgian Research Centre for Application of Steel (OCAS), is a joint industry project and part of the Carbon Trust’s Offshore Wind Accelerator (OWA). The project ‘Improved Fatigue Life of Welded Jacket Connections (JaCo)’, launched in 2017 and concluded at the end of 2023. In addition to showing the possible benefits of robotic welding the JaCo project also showed the efficacy of accelerated fatigue testing method developed by OCAS, which is around 20 times faster than conventional fatigue testing methods. Fatigue is a critical design factor for offshore wind foundations, which represents a large proportion of a wind farm’s CAPEX.

Marc Vanderschueren Head of Business Development at OCAS said: “The importance of JaCo is twofold: the project has fatigue tested large-scale offshore foundation specimens, and the results have established new ground towards successful implementation of robot welding in jacket node fabrication.” Offshore wind jacket foundations, used for deeper water and larger turbines, are currently welded manually, however, if the jackets were robotically welded industry-wide it could potentially improve weld quality and the consistency of the welds.

Ultimately, this could lead to an increase in production and standardisation, with less steel needed, resulting in lighter structures – cutting costs and carbon emissions. This is particularly important as according to the IEA, an additional 70-80GW of offshore wind capacity needs to be installed globally every year from 2030 to achieve Net Zero by 2050. James Sinfield, Technology Acceleration Manager at the Carbon Trust said: “The results from JaCo strongly suggest that automation can play a crucial role in the accelerated deployment of offshore wind, with automated robotic welding proving at least as good as — and often better than — manual welds.

“The project has exceeded our initial expectations, and results will enable the industry to produce structures that could last longer or potentially weigh less than existing foundations. Not only that, but the method pioneered by OCAS and tested via the JaCo project speeds up the testing process producing results equivalent to traditional hydraulic fatigue testing. “This is good news for the Net Zero transition and demonstrates the power of collaboration.

The combined efforts of our industry partners and trusted experts were pivotal to the success as they helped shape the project’s direction and overcome challenges, along with significant input and engagement from the supply chain.” Before robotic welds could be rolled out industry-wide, their fatigue performance needs to be better understood such that guidance for fabricators can be developed and for understanding how the new welding techniques may impact the existing standards. This phase of the JaCo project represents the first stage of this process, with extensive mechanical testing carried out on 26 large-scale geometries to prove the consistency of robotic welding.

The next stage will require work with the certification bodies to translate the JaCo results into industry-wide acceptable practice, including creating industry guidelines and clarifying the conditions in which robotic welding outperforms manual processes. This will help with adoption of robot welding and the new fatigue testing methodology throughout the sector. JaCo is led by the OWA and OCAS, in partnership with developers EnBW, Equinor, ScottishPower Renewables, Ørsted, Siemens Gamesa Renewables, Shell, SSE and Vattenfall. The Scottish Government, European offshore wind supply chain and three certification bodies are also involved.

Source: Offshore Wind Accelerator (OWA)

Subscribe to the free Maintworld newsletter here!

Carbon Fiber Market Size to Grow USD 16.0 Billion by 2032 at a CAGR of 11.4%

The adaptability and broad acceptance of carbon fiber are key factors driving its market expansion, as are ongoing research and development initiatives targeted at streamlining production procedures, cutting expenses, and identifying new uses.

Over the course of the forecast period, the Europe carbon fiber market is expected to develop at the highest CAGR of 11.7%, accounting for 36% of the global carbon fiber market share in 2022. This is because Germany is renowned for its cutting-edge manufacturing and technological know-how.

Type-wise, the continuous carbon fiber segment led the worldwide market in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 11.4% over the forecast period. Based on the end-use sector, the aerospace and defense category generated the highest revenue in 2022 and is expected to rise at a compound annual growth rate (CAGR) of 10.6% during the projection period. Based on raw material, the PAN-based carbon fiber segment had the largest share of the worldwide market in 2022 and is expected to increase at a compound annual growth rate (CAGR) of 11.4% over the forecast period.

Because of its high strength, low heat expansion, moisture absorption, lightweight, specific strength, ease of use, and thermal conductivity, PAN-based carbon fiber composites are favoured for usage in the aerospace sector. Form-wise, the composite carbon fiber category was the biggest source of revenue in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 11.4% over the course of the forecast period. The use of carbon fiber reinforcement in composite materials is referred to as composite carbon fiber. The carbon fiber market is being driven ahead in large part by the aerospace sector. Because of its remarkable strength-to-weight ratio, carbon fiber is a perfect material for aviation parts. Carbon fiber composites are widely used in the construction of aircraft structures as a result of the aerospace industry’s constant quest for increased fuel economy and decreased carbon emissions.

The rising focus on automobile lightweighting projects is one of the main drivers of the carbon fiber market’s expansion. The application of carbon fiber composites in automotive body panels and chassis not only lowers the total weight of the vehicle but also improves performance and fuel economy, which helps drive market growth. Because carbon fiber composites are strong, rigid, and resistant to corrosion, they are widely employed in the manufacturing of wind turbine blades. The usage of carbon fiber in wind energy applications is anticipated to expand, supporting the growth of the market as demand for clean and sustainable energy solutions develops.

Beyond the aerospace and automotive industries, carbon fiber finds use in other industrial sectors as well, which supports the market’s varied expansion. Carbon fiber-reinforced materials are used in industrial settings for components that need to be extremely durable, rigid, and strong. The expansion of the market is mostly due to technological developments in the techniques used in the manufacture of carbon fiber. The introduction of more affordable precursor materials and sophisticated weaving processes, among other ongoing advancements in production methods, have reduced production costs and improved the scalability of carbon fiber manufacturing.

SOURCE: Valuates Reports

Subscribe to the free Maintworld newsletter here!

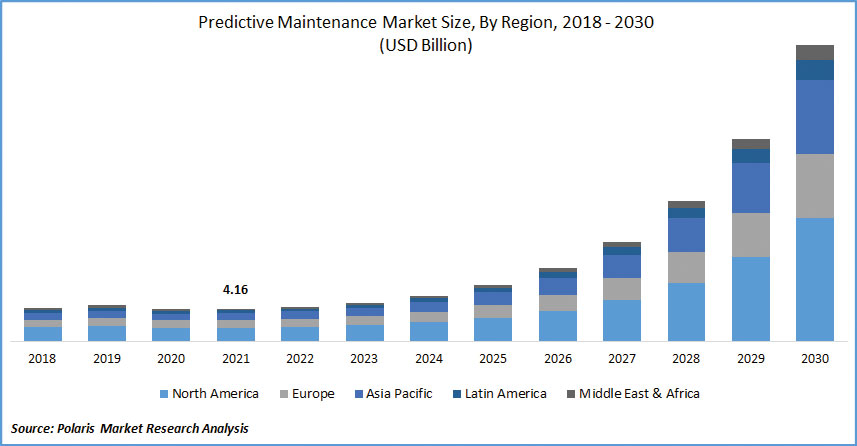

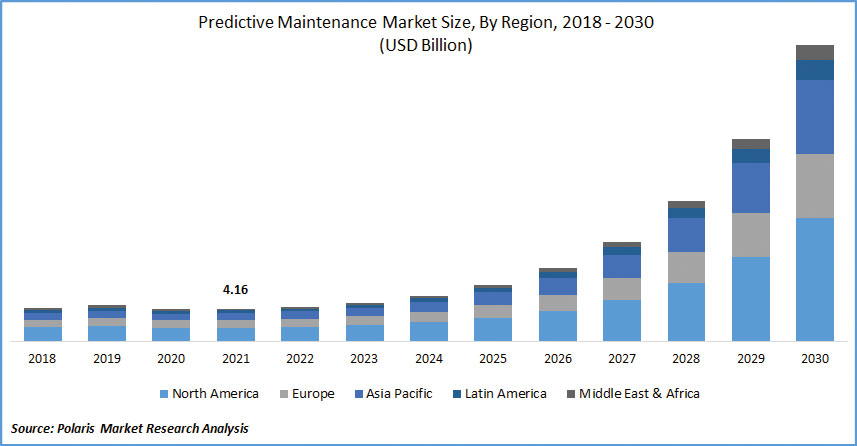

The Predictive Maintenance Market Forecast

The global predictive maintenance market was valued at USD 4.16 billion in 2021 and is expected to grow at a CAGR of 30.9% during the forecast period, according to Polaris Market Research.

Market growth is primarily driven by the need to reduce costs and downtime associated with predictive maintenance. For instance, the data from the U.S. Department of Energy indicates that predictive maintenance is very cost-effective and that it helps an enterprise to gain remarkable results such as a tenfold increase in ROI, 70-75% decrease in breakdowns, 25-30% reduction in costs, and 35-45% reduction in downtime. In addition, the industry enables the technicians to plan and prepare for a repair by taking steps, including shifting the capacity to other equipment or scheduling activity for times with the minimum impact on production.

This results in the elimination of unplanned downtime during the production process. The Covid-19 pandemic disrupted industrial networks and manufacturing, including demand-side shocks along with the supply disruptions that had a negative impact on the industry.

The enterprises were forced to take harsh actions for their staff and employees, as SMEs were shut down, and production & manufacturing facilities were put on hold for a longer period of time. However, this situation has led to significant growth in focus on digital transformation among enterprises. For instance, the pandemic has boosted the need for enhanced manufacturing processes with the integration of technologies such as Machine Learning (ML) and Artificial Intelligence (AI) for the industry.

This has made manufacturing systems more agile and helped manufacturing companies increase their production capacity. Upsurge in investment in predictive maintenance solutions to reduce cost and downtime fuels the growth of the global market.

Investment in predictive maintenance initiatives generates a tangible return on investment (ROI). For instance, predictive maintenance users reported metrics such as 2-6% increased availability, 5-10% inventory cost reduction, and 10-40% reduction in reactive maintenance. In addition, as per the recent study by Deutsche Messe AG and Roland Berger, VDMA 81% of companies are currently devoting time and resources to predictive maintenance subject, while 40% already have confidence that practicing predictive maintenance PdM will be most significant for future business.

This increase in awareness and trust in predictive maintenance solutions is projected to fuel the growth of the industry in upcoming years. On the other hand, the integration of artificial intelligence and machine learning has created lucrative growth opportunities for the predictive maintenance industry. An increasing number of customers are using such solutions powered by AI to help shift from a reactive to a proactive approach. In addition, the market players are actively introducing new AI-enabled solutions. For instance, in September 2020, TeamViewer, a provider of remote connectivity solutions, launched TeamViewer IoT software, an AI-supported.

Subscribe to the free Maintworld newsletter here!

A New Optical Metamaterial Makes True One-Way Glass Possible

Using a new approach, researchers at Aalto University in Finland have been able to design a metamaterial that has so far been beyond the reach of current techniques. Unlike natural materials, metamaterials and metasurfaces can be tailored to have specific electromagnetic properties, which means scientists can create materials with features desirable for industrial applications.

The new metamaterial takes advantage of the nonreciprocal magnetoelectric (NME) effect. The NME effect implies a link between specific properties of the material (its magnetization and polarization) and the different field components of light or other electromagnetic waves.

The NME effect is negligible in natural materials, but scientists have been trying to enhance it using metamaterials and metasurfaces because of the technological potential this would unlock. ‘So far, the NME effect has not led to realistic industrial applications.

Most of the proposed approaches would only work for microwaves and not visible light, and they also couldn’t be fabricated with available technology,’ says Shadi Safaei Jazi, a doctoral researcher at Aalto. The team designed an optical NME metamaterial that can be created with existing technology, using conventional materials and nanofabrication techniques.

The new material opens up applications that would otherwise need a strong external magnetic field to work – for example, creating truly one-way glass. Glass that’s currently sold as ‘one-way’ is just semi-transparent, letting light through in both directions. When the brightness is different between the two sides (for example, inside and outside a window), it acts like one-way glass. But an NME-based one-way glass wouldn’t need a difference in brightness because light could only go through it in one direction.

Subscribe to the free Maintworld newsletter here!

Latest